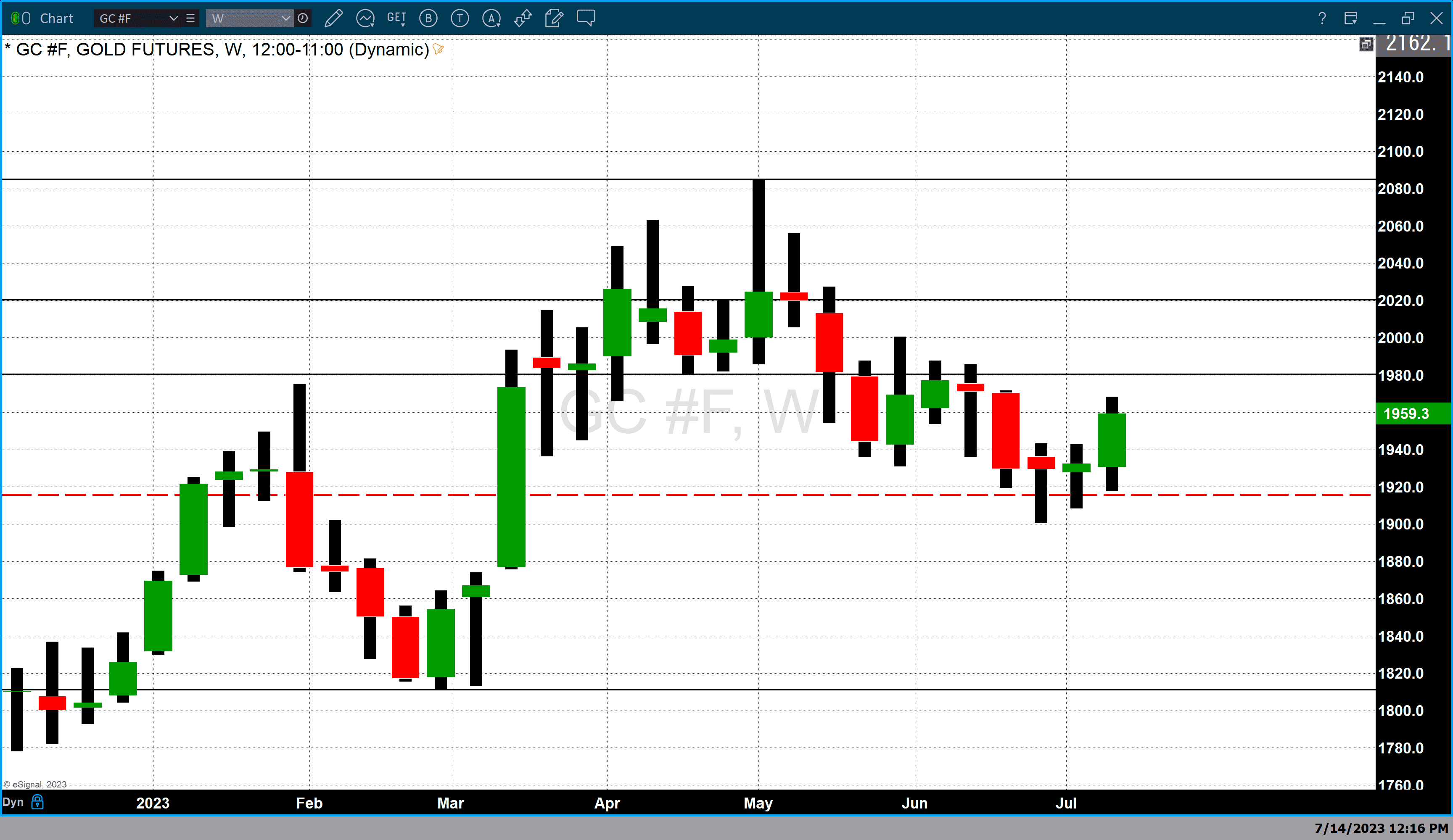

Gold ends the week with fractional gains which are about equal to dollar’s decline

Unquestionably, gold has had an exceptional week rising dramatically after the release of last month’s CPI index earlier this week. However, market participants must be laser-focused on gains or losses as they pertain to dollar strength or weakness. This is because the dollar has been the largest influence on daily price change. Over the last week, the dollar has dropped considerably. After six consecutive days of lower pricing, today was the first day that the dollar index closed above its opening price and above yesterday’s close after hitting the lowest low of this correction and the lowest point since April 2022.

This is what we have seen all week, on the surface traders are witnessing gold gain value. However, at least this week during daily sessions that resulted in large gains in gold had a major component was dollar weakness. After five consecutive days in which gold gained value today, gold closed lower on the day. As of 6 PM EDT, the most active August contract of gold futures is currently trading down $4.50 or 0.23%. Concurrently the dollar is trading fractionally higher up 0.17% taking the index to 99.63. In other words, a large percentage of today’s price decline in gold can be directly attributed to dollar strength.

Spot gold is currently fixed at $1954.30 after factoring in today’s decline of $5.70. The decline in physical gold is the result of a combination of dollar strength and fractional selling by traders. Dollar strength resulted in gold declining by $3.90 in addition to traders providing fractional selling pressure taking physical gold lower by another $1.80.

Yet the root cause of price changes day-to-day in gold and the dollar are intrinsically tied to the monetary policy of the Federal Reserve and other global central banks. As market sentiment changes concerning when the Federal Reserve will conclude its series of aggressive rate hikes, and even more importantly when the Federal Reserve will begin to reduce rates rather than raise them. According to recent statements by Federal Reserve officials they expect that they will implement two more quarter percent rate hikes this year. Furthermore, multiple officials have expressed the belief that they will not begin a period of monetary or rate reduction until the first or second quarter of next year.

The latest data has indicated that inflation is diminishing in both headline data and the Federal Reserve’s preferred component, data from the core CPI which omits volatile items such as food and energy costs. However, core inflation is still elevated more than double their target goal which is 2%. That being said, recent articles have expounded on the idea that the Federal Reserve will pivot its monetary policy from extremely aggressive to very accommodative this year. While there are no statements by any Federal Reserve official confirming that belief investors tend to hear what they want to hear.

In the case of the current persistent inflation that exists globally, it is not just the Federal Reserve which is been aggressively raising rates but central banks globally have been following suit. This makes it much less likely that the Fed will pivot to an accommodative policy without having the data that supports that the Federal Reserve is on a strong and reliable path to reach its target.

For those who would like more information simply use this link.

Wishing you as always good trading,

Gary S. Wagner

Add comment