The “Silver Sizzler” Situation: A Perfect Storm for 2026

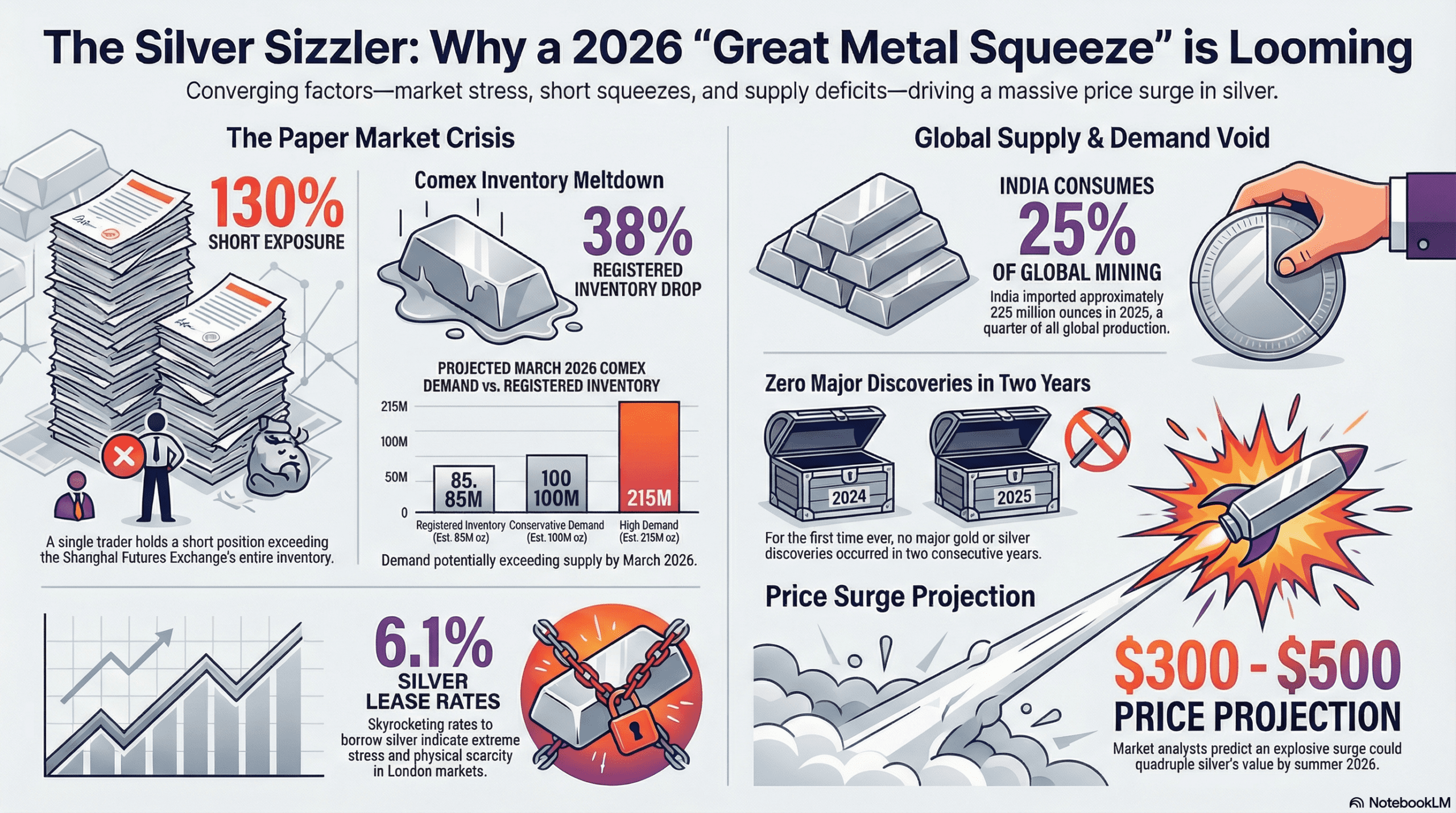

The global silver market is currently facing a convergence of unprecedented supply constraints and explosive demand, creating what is described as a potential “Great Metal Squeeze” of 2026. The situation is defined by a disconnect between the “paper” markets in the West and the physical demand in the East.

1. The “China Syndrome” and Short Squeeze Potential A massive naked short position held by a trader identified as “Mr. Beyond” (approx. 15 million ounces or 450 metric tons) has been exposed and frozen by Chinese regulators. This position exceeds the entire inventory of the Shanghai Futures Exchange. Because the trader must eventually cover this short by buying back physical metal that may not exist in the vaults, analysts predict a violent “short squeeze” similar to the Volkswagen or Nickel market events. Coinciding with this, Shanghai silver inventories recently plunged by nearly 20% in a single week.

2. Western Market Stress (COMEX Breakdown) Signs of systemic stress are visible in Western markets. Silver lease rates in London have spiked to 6.1%, and the market has moved into “backwardation” (where spot prices exceed futures prices), signaling an acute shortage of physical metal. Simultaneously, the COMEX “registered” silver inventory—metal available for delivery—has plummeted by 38% since October. With March 2026 delivery requests potentially exceeding 100 million ounces against a dwindling supply of roughly 85 million ounces, a failure to deliver is considered a possibility.

3. Relentless Global Demand Demand is being driven by India, which imported an estimated 225 million ounces in 2025—roughly 25% of all silver mined globally. Furthermore, Indian banks are set to allow silver to be used as collateral for loans starting in April, effectively monetizing the metal and likely increasing hoarding.

4. The Supply Cliff On the supply side, the mining industry is facing a crisis of discovery. For the first time in recorded history, there have been zero major gold or silver discoveries globally for two consecutive years. Industry executives estimate it will take until 2030 to meaningfully increase production.

Outlook Market analysts, including Michael Oliver (the “Silver Swami”), predict that these pressures could drive silver prices to 300–500 per ounce by early summer 2026.

——————————————————————————–

Suggested Actions and Research

Based on the outlined situation, the following actions and research are suggested for investors:

• Accumulate Physical Metal: The source strongly advocates for holding physical silver rather than paper contracts (ETFs or futures), which are subject to counterparty risk during a squeeze. The “freshness” of bars (directly from mints) is highlighted as a way to ensure secure ownership.

• Investigate Mining Stocks: With the price of underlying metals poised to rise, development-stage companies with verified deposits in safe jurisdictions (e.g., Canada) are suggested as high-potential leverage plays.

• Monitor Arbitrage Spreads: Research the price difference between the Shanghai Gold Exchange (SGE) and Western spot prices. A widening spread indicates the East is draining physical supply from the West.

• Track COMEX Data: Closely watch the “Open Interest” versus “Registered Inventory” for the March 2026 delivery contracts. High delivery demands against low inventory will be the immediate trigger for a price explosion.

Disclaimer: Any information shared in this video should not be construed as investment advice or a recommendation to buy or sell any company stock, meme coin or any other investment product (informational purposes only). Ron may receive compensation from affiliate links and discount codes provided. The information provided on this channel is for general informational purposes only. Bullion Store Ltd. assumes no responsibility for errors or omissions in the content or for any actions taken based on the information provided.

Add comment